A Strong Economy or Looming Recession?

Impending signs of “doom” lurking around the corner sent U.S. stock markets into a tailspin this week, falling roughly 4 percent at their lowest intra-day point. Volatility and downward pressure has been a relatively consistent theme for the Dow Jones Industrial Average, the S&P 500 index and the Nasdaq Composite Index in recent weeks as oil prices have taken a dive, the U.S. and China continue to negotiate trade and tariffs, and whispers of recession could be heard around the marketplace.

Oil Prices

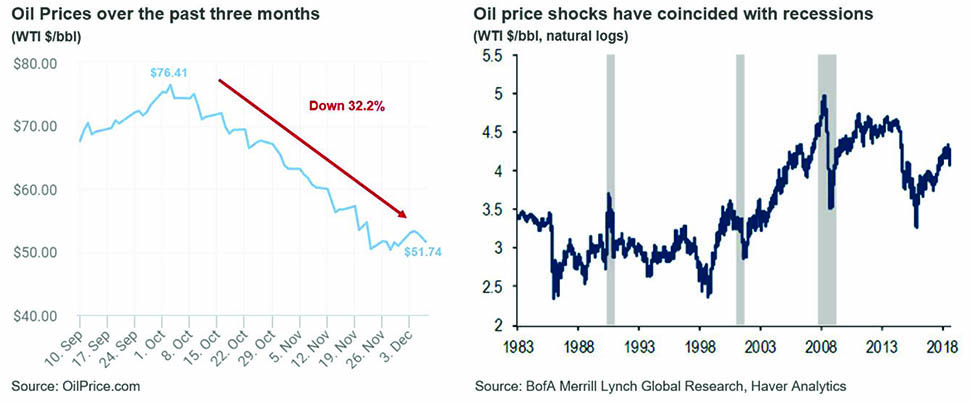

Oil has taken a dive during the fourth quarter of 2018, with West Texas Intermediate (WTI) prices falling from above $76 per barrel on Oct. 6 to just over $51 per barrel on Dec. 6. This sizable drop in crude has fueled fears of recession by many market followers given the strong historical connection between oil price shocks and economic recessions. In addition, correlations between crude oil prices and stock markets have been uncharacteristically high for much of 2018 – close to 0.80.

Oil prices have spiked prior to most of the recessions dating back several decades. In addition, analysts from Bank of America–Merrill Lynch believe that the Great Recession “might not have been as dire absent the oil price shock (Hamilton 2008). That said, an increase in oil prices this time-around may not be as damaging as the U.S. has become a much bigger producer of oil and, in turn, less reliant on crude imports.”

While oil prices have historically been driven by demand, markets now appear to be primarily driven by supply – specifically fears of oversupply. This is because many believe that U.S. technological advances in hydraulic fracturing and horizontal drilling over the last decade have changed the price dynamics of oil and gas. According to estimates from the Federal Reserve, the U.S. is expected to produce approximately 11.2 million barrels of oil per day by the end of 2018.

Recently, Organization of Petroleum Exporting Countries (OPEC), one of the world’s largest suppliers of crude oil, has been fanning fears of a glut in global oil supply. The group of oil-producing countries has been adhering to self-imposed production cuts over the past year, but these production caps are set to expire at the end of the year.

Although energy prices rallied in September with traders bracing for renewed U.S. sanctions on Iran coupled with President Trump's threat to sanction foreign firms buying Iranian crude, October forecasts had suggested slower demand growth just as output from top producers were rising. Cartel member adherence to OPEC production cuts had been a support for the last year; however, the cuts expire at year’s end. OPEC-member countries met this week in Vienna to determine whether these production curbs would be renewed, but the meeting concluded without a final decision being made.

U.S./China Trade Talk

A significant amount of media attention has been placed on ongoing trade discussions between China and the U.S. – the world’s largest economies and trade partners. Even though leaders from the two countries appear to have come to a truce, there’s a significant likelihood tariffs on certain Chinese goods are on the horizon in 2019.

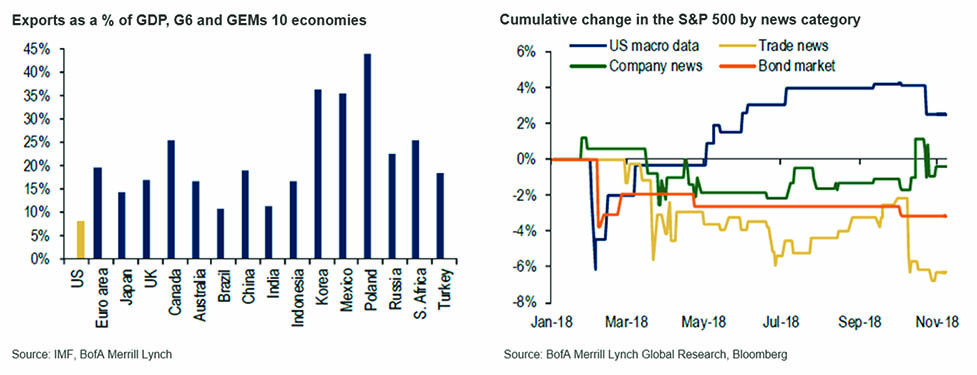

While the Trump Administration’s approach to trade negotiations will certainly continue to grab headlines, it’s important to remember that the eventual outcome will likely have a limited effect on the U.S. economy. The chart on the left below illustrates that the U.S. economy is much less reliant on exports than other major countries around the world. In a November 14, 2018 economic viewpoint from Bank of America–Merrill Lynch¹, analysts highlighted that, “Compared to other large economies the U.S. has limited exposure to global demand. Recent undulations in the global backdrop, from the soft patch of 2015-16 to the coordinated pickup in 2017, suggest that a slowdown in demand for U.S. exports would not be large enough to cause a recession.”

Considering this loose correlation, U.S. stock markets have moved disproportionately downward when trade talks have hit the front page. The chart on the right above from Bank of America–Merrill Lynch shows that “Trade News” has had a stronger downward effect on the S&P 500 Index than company news, the bond market and macroeconomic data on the U.S.

Inversion of the U.S. Treasury Yield Curve

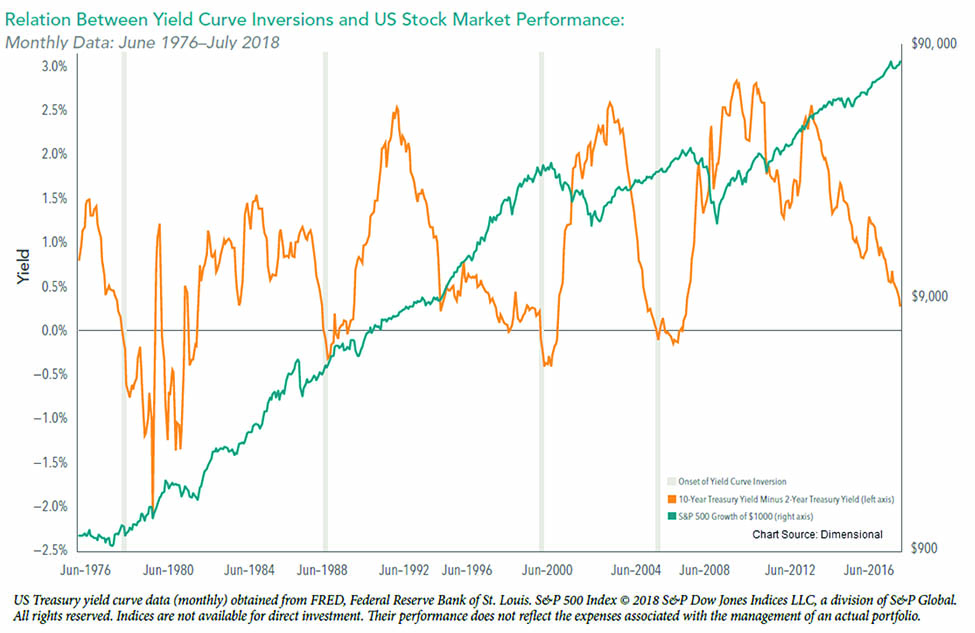

We also reached a technical flashpoint this week with a mild inversion in parts of the U.S. Treasury yield curve. As of the writing of this piece, the 2-year U.S. Treasury is yielding slightly more than the 5-year U.S. Treasury yield. The widely followed 2-10 year U.S. Treasury spread is 13 basis point currently.

While some market pundits believe this leading indicator is a sign that a recession is likely to begin in the near future, that’s not necessarily the case. Recent research from Dimensional, shows that the link between periods of yield inversion and negative stock market returns isn’t as strong as many think.

The U.S. Treasury yield curve inverted in February 2006 but the S&P 500 posted positive returns for the following 12-months. In addition, the yield curve returned to a positive slope in June 2007 prior to the market’s downturn beginning in October 2007. Dimensional’s research shows that returns (in local currency) of major indices for five of the largest developed nations (U.S., UK, Australia, Germany and Japan) were higher 86 percent of the time 12 months later and 71 percent of the time after 36 months.

The company sums up its findings with the following, “If an investor interpreted the inversion as a sign of an imminent market decline, being out of stocks during the inverted period could have resulted in a substantial opportunity cost. And if the same investor invested in stocks once the curve returned to a positive slope, they would also have been exposed to the stock market weakness that followed”²

Positive Indicators of a Strong Economy or Looming Recession?

The impossible question many investors are likely asking themselves is – are we headed for a recession? The answer is…it depends on where you look.

The National Bureau of Economic Research (NBER), the organization responsible for officially declaring a recession, defines a recession as a “significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.

By those measures, there’s certainly some positive indicators of a strong economy. While corporate debt is close to an all-time high during a business cycle, interest coverage ratios remain solid. Company earnings have been strong this year and unemployment in the U.S. continues to be low.

Economic data continues to show strength for the American consumer, which is important as consumers drive a large portion of the market. Consumers are continuing to spend during this holiday season and balance sheets look healthy with outstanding household debt as a percentage of total GDP around 79 percent – far below the peak levels of 125 percent seen in 2009.

Despite this strength, the consensus estimate of the probability that we will experience a decline in GDP a year from now has reached its highest level since 2008 according to the Survey of Professional Forecasters and reported by Goldman Sachs.³ This means we likely won’t know the answer to the recession question until this time next year.

In the meantime, Wall Street and Main Street are keeping both eyes on the Federal Reserve and rising interest rates. While nobody knows the Fed’s next move, a report from Capital Economics out this week said the company thinks “the Fed will raise rates twice in the opening six months of 2019, taking the fed funds target range to between 2.75 percent and 3 percent.”⁴

Recession or not, we believe clients should continue to follow their long-term financial plans and revisit their goals and objectives with their trusted financial advisors if feeling uncertain about the future. If the current market volatility persists, continuing to dollar cost average into the market at lower prices can be an opportunity to positively affect long-term performance.

Economic and market cycles come and go, but a solid, long-term financial plan revisited regularly can help withstand the test of time.